Is Crypto Staking Halal?

The rise of cryptocurrency has sparked numerous innovations in the digital finance world, including staking, a key method for earning passive income in blockchain ecosystems. Staking allows crypto asset holders to lock their assets to support network operations, such as transaction validation, in exchange for rewards. However, for Muslims in Malaysia, a critical question arises: does staking comply with Shariah principles? This article explains what staking is, how it works, and shariah perspective from sharlife.

What Is Staking?

Staking refers to the process where cryptocurrency holders, such as those owning Ethereum (post-Proof-of-Stake transition), Solana, or Cardano, lock a portion of their assets in a digital wallet to support blockchain network operations. In return, they receive rewards in the form of new coins or transaction fees. Staking is an alternative to mining in Proof-of-Work systems, which require high energy consumption. Proof-of-Stake (PoS) and Delegated Proof-of-Stake (DPoS) systems rely on staking, where validators are chosen to verify blocks based on the amount of crypto staked. This makes staking more environmentally friendly and efficient, positioning it as a popular choice in modern blockchain ecosystems.

Proof of Stake (PoS)

In PoS blockchains, creating and validating new blocks is called forging or minting. The PoS algorithm selects validators from a pool of crypto holders who have staked their assets. The more crypto staked, the higher the chance of being selected as a validator. Examples include Ethereum (ETH), Cardano (ADA), and Solana (SOL).

Delegated Proof of Stake (DPoS)

DPoS is an evolution of PoS, introducing a democratic element where stakeholders elect delegates to validate and forge blocks. This system is designed to be more efficient and scalable, requiring fewer validators. Examples include EOS (EOS) and TRON (TRX).

In summary, staking involves two key elements:

-

Asset Locking: Owners lock their coins for a specific period, either flexibly or fixed.

-

Rewards: Rewards are distributed based on the staked amount, lock-up period, and the network’s consensus algorithm.

3. How Does Staking Work?

Staking operates within blockchains using the Proof-of-Stake (PoS) consensus mechanism. Below are the basic steps of how staking functions:

-

Asset Locking: Crypto holders lock a certain amount of coins in a compatible digital wallet for a specific blockchain protocol. For example, in Ethereum 2.0, a minimum of 32 ETH is required to become a full validator, though staking pools allow participation with smaller amounts.

-

Network Role: Locked assets support blockchain operations, such as validating transactions or creating new blocks. Validators are randomly selected based on the amount staked and other factors, like lock-up duration.

-

Rewards and Risks: Participants receive rewards in the form of additional coins or transaction fees. In Islamic finance terms, these rewards are comparable to dividends on investment accounts, hibah on qard savings accounts, or profits from tawarruq fixed deposit accounts. However, risks include slashing (penalties for validator technical failures) or losses due to crypto price volatility.

-

Flexibility: Some platforms allow flexible staking (assets can be withdrawn anytime), while others require locking for a fixed period.

This process requires technical understanding and readiness to accept market risks, which are key points in the Shariah perspective.

Is Staking Halal? A Shariah Perspective

Before discussing staking, it’s important to note that Islamic scholars and Shariah regulatory bodies, such as the Shariah Advisory Council of the Securities Commission Malaysia (SAC SC), recognize digital assets or cryptocurrencies as “mal” (property with value) under Shariah perspective.

At its 233rd (June 29, 2020) and 234th (July 20, 2020) meetings, the SAC SC distinguished between two types of digital assets:

-

Technology-based assets, such as Bitcoin (BTC), Ethereum (ETH), and Solana (SOL).

-

Ribawi-based assets, such as gold, silver, and fiat currencies.

This Shariah analysis focuses on technology-based crypto assets, which are not considered currencies. Therefore, the rules of bay’ al-sarf (currency exchange) do not apply.

Shariah Analysis of Staking Structure

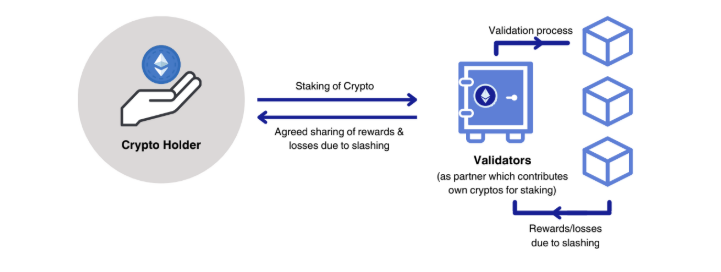

In staking, crypto holders lock their assets to support transaction validation in a blockchain, receiving rewards in return. Two primary Shariah contracts can be used to understand this structure:

- Musyarakah (Partnership)

According to the Bank Negara Malaysia (BNM) Policy Document (2015) and AAOIFI, musyarakah is a partnership where two or more parties contribute capital and share profits and losses.

In staking:

-

Crypto holders and validators pool their crypto to be selected as validators.

-

If selected, they receive rewards (typically new coins or transaction fees).

-

Rewards are distributed based on an agreed-upon ratio.

For exchange platforms like Binance or Coinbase:

-

They may charge fees (e.g., 10% on Binance, up to 35% on Coinbase).

-

This can be structured as:

-

Ijarah al-a’mal (service fees),

-

Ju’alah (rewards for achieving results), or

-

Musyarakah if they share profits and bear some losses.

-

On the issue of contributing cryptos in the staking process not cash for the partnership, both BNM Policy Document and Shariah Standard No. 12 by AAOIFI allows the capital contributed to be in- kind or in the form of commodities or labour which make the Shariah contract suitable to be the basis of the transaction.

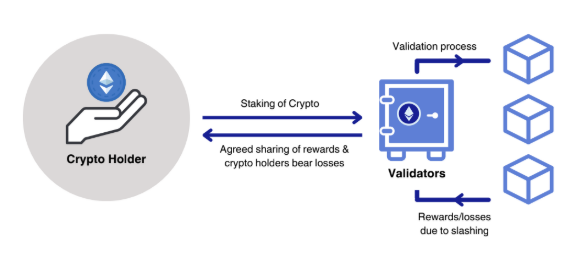

- Mudarabah (Investment Partnership)

Mudarabah is a contract between Rabbul Mal (capital provider) and Mudarib (manager). Profits are shared, but losses (not due to negligence) are borne solely by the rabbul mal.

In staking:

-

Crypto holders are the rabbul mal, providing capital.

-

Validators are the mudarib, performing validation tasks.

-

Rewards are shared based on an agreed ratio, while losses (e.g., slashing or downtime) are borne by the crypto holder.

For exchange platforms:

-

They can act as rabbul mal if they provide capital.

-

They can act as mudarib, sharing rewards with validators.

-

Alternatively, they may only charge service fees (ijarah or ju’alah).

On capital contribution, BNM allows in-kind capital, even intangible assets, and AAOIFI permits tangible non-cash assets. Thus, there is no issue with using crypto as capital in a mudarabah venture.

Conclusion from Shariah Analysis

Based on the evaluation of staking’s general structure, staking is deemed permissible (halal) under Shariah, aligned with the fiqh principle:

“The default ruling for contracts and conditions is permissibility and validity.”

Staking, whether done directly with validators or through platforms like Binance and Coinbase, shows no clear violation of Shariah principles, particularly in avoiding riba (usury), gharar (excessive uncertainty), and maysir (gambling), especially for technology-based digital assets not classified as ribawi (e.g., gold or fiat currencies).

Although Shariah contracts are not explicitly used in current staking offerings, fiqh principles emphasize:

“The ruling of a matter depends on its intent and substance, not merely its form or wording.”

However, to build confidence and clarity for Muslim crypto holders, explicitly adopting Shariah contract structures is encouraged to ensure transparency and fairness in defining roles, reward distribution, and risk or negligence management.

Conclusion

Staking plays a vital role in the crypto ecosystem, serving as a source of passive income (rewards) while supporting blockchain network security and efficiency. As the industry matures, staking mechanisms will become more sophisticated, focusing on broader user participation and network stability. For Muslim crypto holders interested in staking, it is crucial to thoroughly understand the staking process, associated risks and rewards, and relevant Shariah guidelines and requirements.